Accounting Cycle: Phases, Benefits and Need

Most businesses follow this eight-step accounting cycle to ensure to ease the process of financial accounting. It ends with the completion of a transactions and is included in the financial statements by the end of a financial year.

In this article, we will discuss the advantages, disadvantages, purpose and phases of accounting.

Table of Contents

What is Accounting Cycle?

The accounting cycle refers to the comprehensive procedure of recognizing, examining, and documenting a company’s financial activities. This routine 8-step method starts with the initiation of a transaction and concludes with its representation in the financial reports and the finalization of the records.

An accounting cycle is a process that is designed to ease the financial accounting of business activities for business owners. It is a sequence of relevant procedures to record, classify and summarise accounting information in an organized manner.

The cycle begins when financial transactions take place. It ends when these transactions are included in the financial statement at the end of an accounting period. These days, these steps are automated through different types of accounting software. However, it is important to know the fundamentals of the accounting cycle phase for understanding the process in detail.

Explore accounting courses

Best-suited Accounting and Control courses for you

Learn Accounting and Control with these high-rated online courses

Fundamentals of Accounting Cycle

The accounting cycle represents a structured sequence of actions that businesses undertake to chronicle and structure their financial activities, culminating in the creation of financial reports. This methodology promotes uniformity, precision, and adherence to accounting standards. Below are the essential phases of the accounting cycle:

- Transaction Recognition: The process kicks off with pinpointing economic events like sales, acquisitions, wages, and more. Every such event influences the financial position and is thus documented.

- Journal Entry: After spotting these transactions, they are sequentially documented in a journal, a process commonly termed “journalizing”. Standard details in an entry encompass the transaction date, involved accounts, monetary values, and a concise explanation.

- Transferring to the Ledger: Subsequent to journalizing, these entries are moved or “posted” to the main ledger. This ledger aggregates accounts, showcasing the evolution in their values.

- Drafting an Initial Trial Balance: Once a period’s transactions are all posted, a preliminary trial balance is drawn up. It lists every account and its balance, verifying the equilibrium between debit and credit values.

- Incorporating Adjustments: Some financial activities might not be instantly journaled. Events like asset depreciation or acknowledging outstanding expenses mandate end-of-period adjustments. These adjustments align with the principles of revenue recognition and expense matching.

- Compiling a Revised Trial Balance: Post the inclusion of adjustments, an updated trial balance is drafted, confirming the balance between debits and credits.

- Formulating Financial Reports: Leveraging the revised trial balance, the firm formulates its financial reports. This usually encompasses the profit and loss statement, balance sheet, and statement of cash flows.

- Finalizing Entries: As an accounting period concludes, transient accounts like revenue, costs, and dividends are finalized to a lasting equity account, frequently termed “Retained Earnings”. This act zeroes out the transient accounts, priming them for the forthcoming period.

- Drafting a Closing Trial Balance: This concluding phase ensures that post the finalizing entries, the debit and credit values remain balanced. This balance only considers lasting accounts since transient ones have been zeroed out.

- Reversal Entries: Within certain accounting frameworks, specific adjustments done in a given period might necessitate reversal in the succeeding period. This guarantees the unique recording of transactions.

Read Later

Read LaterWhy do businesses use this cycle?

Businesses need an accounting cycle due to the following reasons:

- Businesses use the accounting cycle for recording and preparing accurate financial statements.

- This cycle helps business owners in closing their books for an accounting period.

- It also helps with the information required for performing financial statement analysis and managing the business.

Explore accounting courses

Advantages of Accounting Cycle

The following are the benefits of an accounting cycle:

- Measure effectiveness: Through the accounting cycle, businesses can measure the effectiveness of a financial strategy that has been implemented in the past.

- Accurate financial statements: The accounting cycle helps in the generation of accurate financial statements when the cycle is followed till the end.

- Become compliant: These are the set of accounting principles and procedures that must be followed in the cycle. This makes the business compliant with accounting standards.

Disadvantages of Accounting Cycle

- Accounting follows the concept of money measurement. This means that non-financial transactions are not recorded in books of account.

- Since non-financial transactions are not recorded, the actual financial situation of the company is not portrayed.

- The accounting information of an entity is influenced by methods opted by accountants. It may get impacted by the inventory valuation method, depreciation method and treatment of the revenue and capital expenses.

Explore free accountant courses

Importance of Accounting Cycle

The accounting cycle helps companies in the following manner:

- Helps in ensuring that the entire money that is coming in or going out of the business is accounted for.

- Every transaction is analyzed and recorded which makes the system more transparent and accountable.

- Ensures that the data is organized and accurate.

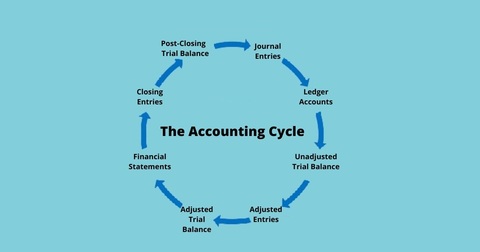

Phases of Accounting Cycle

An accounting cycle has different steps that provide business owners with comprehensive financial performance reporting for analyzing the business. Following are the eight steps in an accounting cycle:

1. Identifying Transactions

The first step is identifying transactions. Every transaction in the business must be properly recorded in the company’s books. This is a process called recordkeeping that is essential for recording every type of transaction.

An accountant records transactions in the accounting system through double-entry bookkeeping with balancing credits and debits. Transactions may be recorded on a monthly or annual basis.

2. Recording Transactions

The second step in this process is recording transactions through the creation of journal entries. If a business wants to record non-routine accounting transactions, it will prepare journal entries for required transactions. This is done through a subsidiary ledger such as accounts receivable.

Point of sale technology is used for identifying and recording transactions. Before recording the transaction, the company must choose whether they want to follow the accrual or cash method. If the company chooses the accrual method, it will require the matching of revenues with expenses to be booked at the time of the sale.

Journal entries help in recording accruals and reversing them in the next period of accounting when the accrual is determined. In case, the business chooses the cash method, then the transaction must be recorded when cash is actually paid or received.

3. Posting

After a financial transaction is recorded as a journal entry, it must be posted to an account in general ledger. This ledger will break down the accounting activities by account. A bookkeeper will be able to monitor financial status by account.

Explore Popular Online Courses

4. Trial Balance

At this step, the accountant will ensure that each transaction is recorded in general ledger. For this purpose, unadjusted trial balance reports are generated from financial records. A trial balance is calculated by the end of an accounting period. This trial balance reflects the company’s unadjusted balance in every account.

The unadjusted trial balance is carried forward in the next phase for testing and analysis. Through this step, accountants can ensure that the total credit and debit balance is equal. This step occurs once the accounting period has ended and transactions have been identified, recorded, and posted to ledger.

5. Worksheet Analysis

At this stage, a worksheet is created to analyze, identify and reconcile adjusting and consolidation entries. Every balance sheet must be reconciled monthly to rectify errors by adjusting journal entries. Compare bank accounting statements with its general ledger cash account.

Reconcile assets and liabilities, inventories, prepaid assets, fixed assets, and retained earnings with general ledger. In the consolidation process of multi-entity companies, income statements and balance sheets should be combined. Transactions that are not with a third party (such as intercompany profit) must be eliminated as worksheet adjustment.

6. Adjustments

At this stage, the bookkeeper makes adjustments which are recorded as journal entries as per the requirement. This helps in correcting errors and reflecting differences noted in reconciling balance sheet accounts.

The total debit and credit balance must be equal after the adjusting entries are entered and posted to the general ledger. To check this, you can run and review the adjusted trial balance report.

7. Generate Financial Statements

After making adjusting entries, financial statements including income statement, cash flow statement and balance sheet are generated. You can generate these statements for monthly or annual accounting periods.

According to the SEC, public companies need quarterly financial reporting. These statements are reviewed and approved by the management before they are issued.

8. Closing the books

This step takes place at the end of the fiscal year. The company closes its accounting cycle by closing its books on a specified date. Closing statements provide reports for the analysis of the company’s performance over the period.

At the end of the accounting period, companies prepare post-closing trial balance reports. They need to ensure that the total credits are equal to total debits. To correctly complete the year-end accounting close process, temporary ledger accounts must be zeroed out.

9. Post-Closing Trial Balance

Once accounts are closed, a final trial balance is created. This confirms that ledger is balanced once closing entries are made. These closing enteries should only consist of permanent accounts with end-of-period balances. It ensures that debits are equal to credits before starting a new accounting period.

Role of Technology in the Accounting Cycle

Technology plays a crucial role in the accounting cycle by streamlining and automating the various steps involved, from recording transactions to preparing financial statements. The use of technology in the accounting cycle can lead to increased efficiency, accuracy, and speed.

1. Use of Accounting Software

Accounting software has functional modules that can be used to record and manage accounting activities, including accounts payable, accounts receivable, journal, general ledger, payroll, and trial balance. It functions as an accounting information system. Software like QuickBooks, Sage, and Xero can automate the process of recording transactions, posting debits and credits, issuing invoices, and monitoring inventories. This can reduce the time required for these tasks and reduce errors.

2. Automation of Accounting Processes

Automation of accounting processes is the use of technology to replace manual, repetitive accounting procedures. For instance, software can be used to automatically reconcile bank statements, manage expenses, calculate taxes, and generate financial reports. Automation can improve accounting data accuracy, reduce the likelihood of errors, and offer accountants more time to work on other crucial tasks.

Conclusion of Accounting Cycle

As technology is advancing, accounting software are replacing traditional methods. This has made the process much easier, more accurate, and less time-consuming. However, it is important to understand the processes on a fundamental level to accurately complete the cycle.

FAQs

Which is the most important output of an accounting cycle?

Financial statements are the most important output of an accounting cycle.

What are ledger books?

Ledger books contain accounts that consist of classified and summarized information from journals as debit and credit.

Name the three types of ledgers.

General, creditors, and debtors are the three types of ledgers.

What is the first step in the accounting cycle?

First step in accounting cycle is identifying and analyzing financial transactions.

How does the accounting cycle end?

The cycle concludes with the preparation of financial statements and the closing of temporary accounts.